Infinite Banking Example: A Simple Breakdown With Real Numbers

See a real infinite banking example with simple numbers. Learn how it works, why people use it, and whether it’s right for you.

Infinite Banking Example: A Simple Breakdown With Real Numbers

Infinite banking is one of those concepts that sounds simple until someone tries to explain it. Most articles either bury you in insurance jargon or make vague promises about "becoming your own bank" without ever showing how it actually works.

So instead of starting with theory, let's start with a real example. Once you see the numbers, the mechanics of infinite banking become much easier to understand. Then we'll break down why people use it, where it works, and where it doesn't.

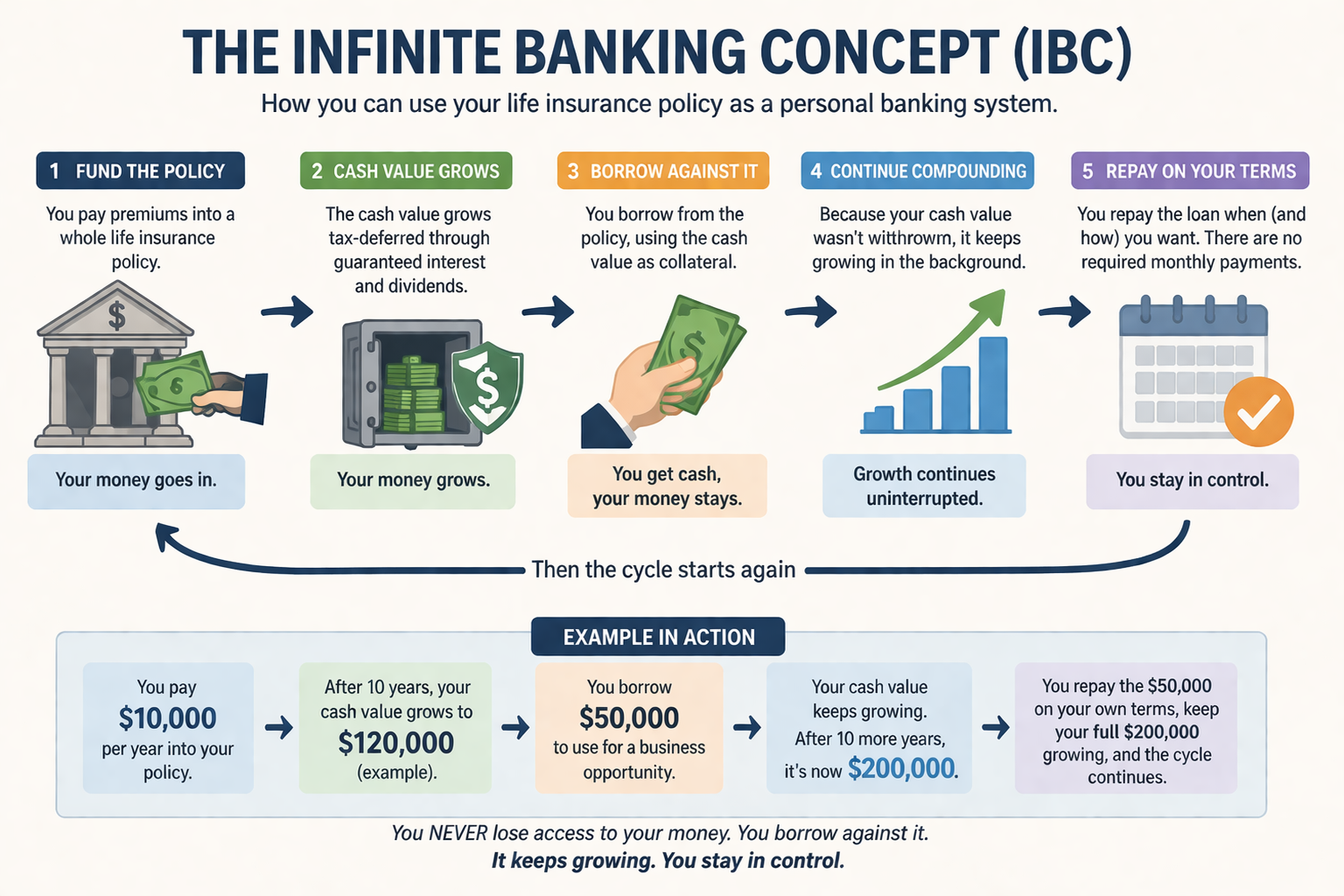

Here’s what’s important to understand:

- John doesn’t withdraw his money—he borrows against it.

- His full cash value continues to grow, even after taking the loan.

- The loan is secured by the policy, not taken from it.

- Over time, his cash value keeps compounding while he uses the money elsewhere.

In simple terms:

- He stores money in the policy.

- The money grows steadily over time.

- When he needs cash, he borrows against it instead of spending it.

- His original money keeps growing the entire time.

A Real Example From An IBC Whole Life Policy

The example above is simplified, but here’s what this looks like in practice using a real policy.

The breakdown below is based on a real example from another author, which you can read in full here → The Case For Infinite Banking

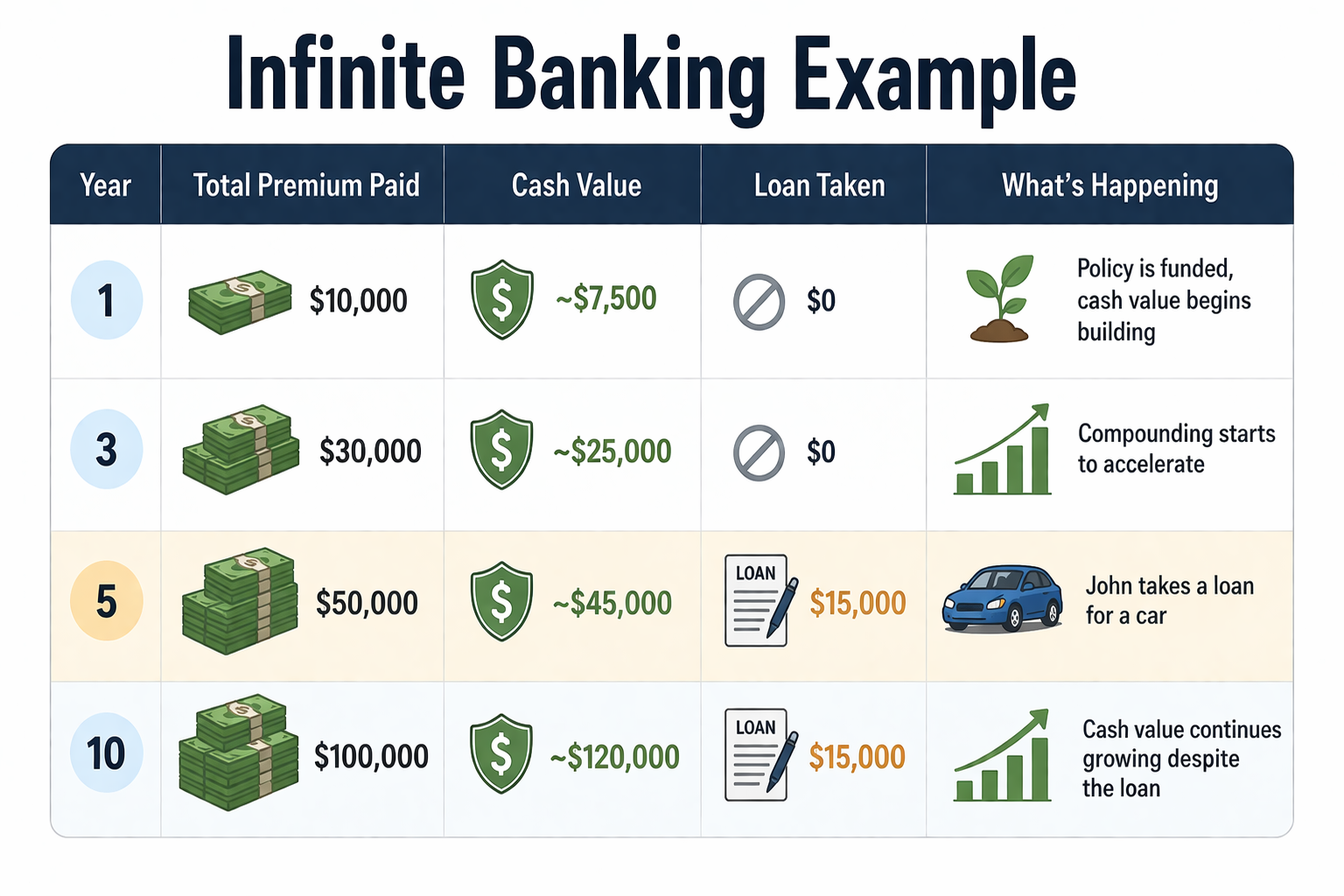

In this case, the policy was set up with a $10,000 annual premium and a death benefit of roughly $500,000.

After funding the policy, a $6,000 loan was taken against it.

Here’s the part most people don’t understand:

Even after taking the loan, the policy's cash value continues to grow as if the money had never been touched.

This is because the loan isn’t taken from the policy—it’s taken against it. The insurance company lends the money using the policy as collateral, while the policy's full cash value continues to compound in the background.

The only thing that changes is the death benefit. If the loan is never repaid, the balance is simply deducted from the amount that would eventually be paid out.

So, in practical terms, $6,000 was accessed while the policy continued to grow. Nothing was liquidated, and nothing interrupted the compounding.

That’s the core idea behind infinite banking:

You can use your money without stopping its growth.

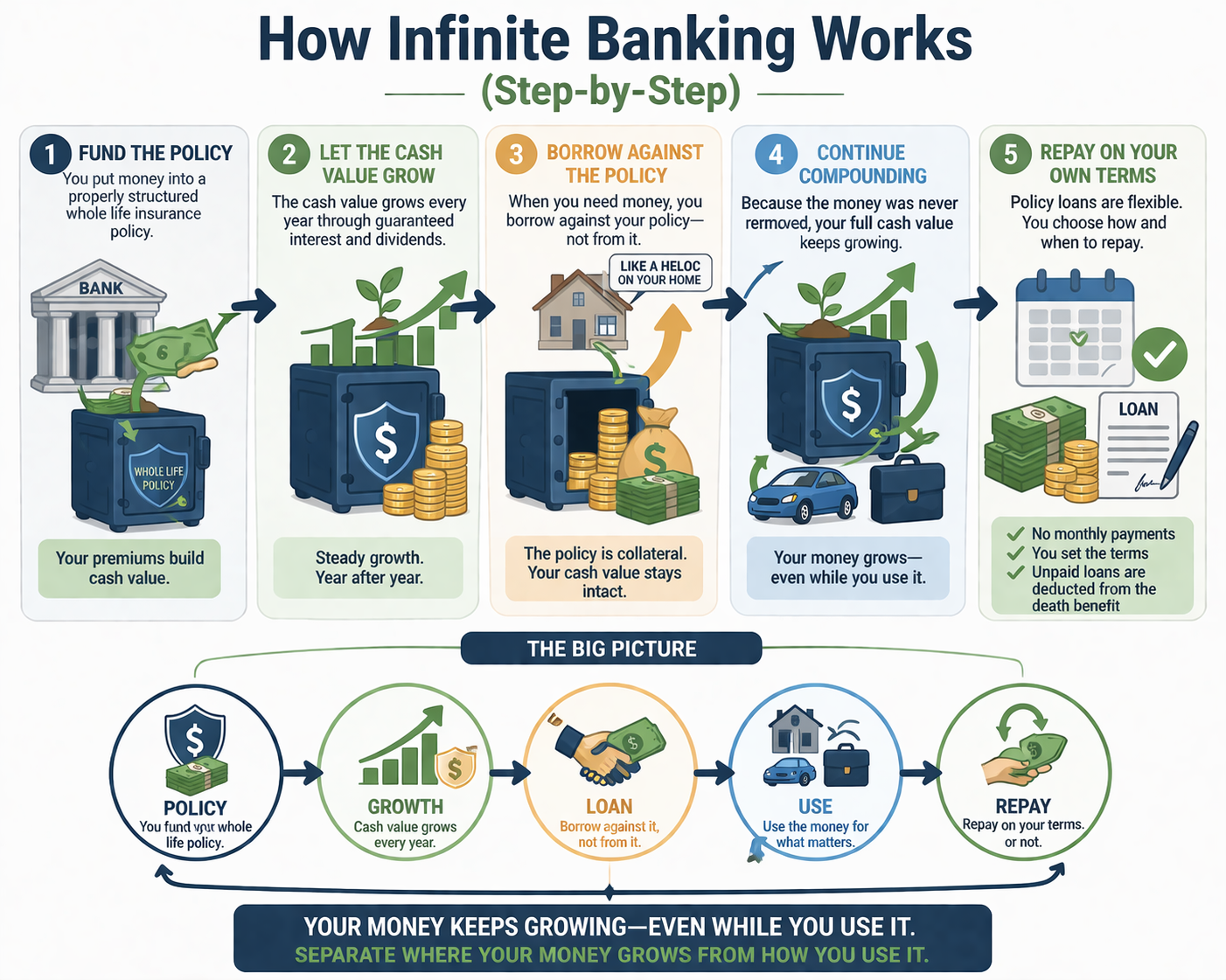

What Is Infinite Banking? (Simple Explanation)

At its core, infinite banking is a way to store and use money more efficiently.

Instead of keeping your money in a traditional bank account, you place it inside a whole life insurance policy that builds cash value over time. That cash value grows steadily each year.

When you need access to money, you don’t withdraw it—you borrow against it.

Because the loan is secured by the policy, not taken from it, your full balance continues to grow in the background.

How infinite banking works in practice

- You store money in a policy

- The money grows over time

- When you need cash, you borrow against it

- Your original money keeps compounding the entire time

The key idea is simple:

It’s not about chasing the highest return. It’s about keeping your money growing while you use it.

Why People Use Infinite Banking

Once you understand how infinite banking works, the next question is: why would someone choose to use it?

At a high level, it’s not about maximizing returns. It’s about improving how your money behaves over time.

Continuous growth, even when you use the money

In most situations, using your money stops it from growing.

If you spend cash, it’s gone.

If you sell an investment, it stops compounding.

With infinite banking, your money continues to grow even after you access it, because you’re borrowing against it—not withdrawing it.

Access to capital without liquidating assets

Instead of selling investments or draining savings, you can access cash through a policy loan.

That means:

- No need to interrupt long-term investments

- No forced timing decisions (like selling in a down market)

- No approval process based on income or credit

You’re using your own capital as collateral.

Stable, predictable growth

The cash value inside a whole life policy grows steadily over time.

It’s not tied directly to the stock market, and it doesn’t fluctuate day to day.

For some people, this stability is the point—not a drawback.

Flexibility in how loans are handled

Policy loans are different from traditional loans.

- There are no required monthly payments

- Repayment timing is flexible

- The loan can be carried indefinitely if needed

This gives you more control over your cash flow.

Tax advantages

The growth inside the policy is generally tax-deferred, and policy loans are not treated as taxable income.

That means you can access capital without triggering a taxable event.

Bringing it together

People use infinite banking because it allows them to:

- Keep their money growing

- Access capital when needed

- Maintain control over how and when they use it

It’s less about chasing the highest return and more about creating a system where your money remains productive at all times.

Pros and Cons of Infinite Banking

Like any financial strategy, infinite banking has trade-offs. It can be powerful in the right situation, but it’s not a perfect fit for everyone.

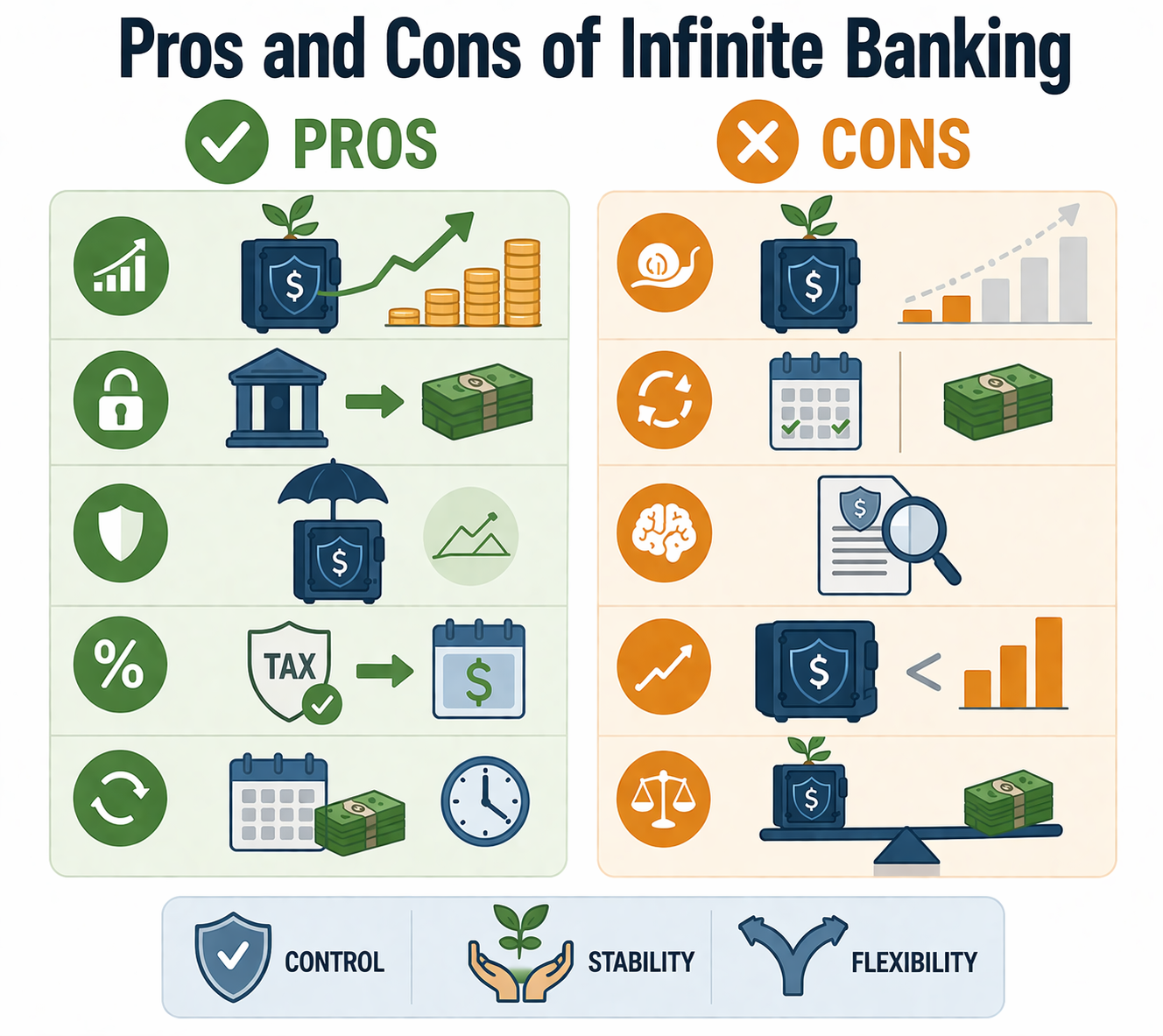

Pros

One of the biggest advantages is that your money continues to grow even when you use it. Because you’re borrowing against the policy instead of withdrawing from it, the underlying cash value keeps compounding over time.

It also gives you access to capital without having to sell assets or rely on a bank. You’re not tied to market timing, and there’s no approval process based on your income or credit.

Another benefit is stability. The growth within a properly structured whole-life policy is steady and not directly tied to market fluctuations. For people who value predictability, this is a major advantage.

There are also tax benefits. Growth inside the policy is generally tax-deferred, and policy loans are not treated as taxable income, which allows you to access capital without triggering taxes.

Finally, policy loans offer flexibility. There are no required monthly payments, and you can choose how and when to repay the loan.

Cons

The biggest drawback is slow early growth. In the first few years, a portion of your premium goes toward fees and insurance costs, which means your available cash value will be lower than what you’ve put in.

It also requires consistency. You need to fund the policy regularly for it to work as intended, especially in the early years.

There’s also complexity. Proper policy design matters, and most people don't fully understand it without guidance.

And while the growth is stable, it’s not designed to compete with higher-risk investments like stocks or real estate. If your goal is maximum returns, this likely won’t be the best standalone strategy.

An honest assessment of infinite banking

Infinite banking works best when you understand both sides.

It offers control, stability, and flexibility—but in exchange, you give up some liquidity early on and accept more modest long-term returns compared to higher-risk investments.

Who Infinite Banking Is For (And Who It’s Not)

Infinite banking can be a powerful tool, but it only works well in the right context.

It’s not something everyone should do—and understanding that upfront will save a lot of frustration.

Who it works well for

Infinite banking tends to make the most sense for people who have consistent income and are thinking long-term.

This often includes:

- People with strong cash flow who can fund a policy regularly

- Business owners who want access to capital without relying on banks

- Long-term savers who value stability over volatility

- Individuals who want more control over how they store and use money

For these types of situations, infinite banking can act as a central place to store capital while still keeping it available for future use.

Who it’s not a good fit for

There are also situations where infinite banking doesn’t make much sense.

It’s usually not a good fit for:

- People who need short-term liquidity

- Anyone who can’t consistently fund the policy

- Those looking for fast or high returns

- People who prefer simple, hands-off financial strategies

Because of the slow early growth and required commitment, it can feel frustrating if your financial situation doesn’t support it.

Frequently Asked Questions About Infinite Banking

Is infinite banking legit?

Yes, infinite banking is a legitimate strategy. It uses the cash value of a properly structured whole life insurance policy. The concept has been around for decades and is widely used, though often misunderstood.

Is infinite banking a scam?

No, but it is sometimes marketed poorly.

Problems usually stem from poorly designed policies or unrealistic expectations. When properly structured and used, the strategy works as intended.

How long does it take for Infinite Banking to work?

It’s a long-term strategy.

In the early years, your available cash value will usually be less than what you’ve paid in due to fees and insurance costs. Over time, the compounding becomes more noticeable, typically after several years.

Can you lose money with infinite banking?

You’re not exposed to market losses as you would be with stocks.

However, you can lose efficiency if the policy is poorly designed or underfunded. The main risk isn't volatility—it’s improper setup and use.

Do you have to pay back policy loans?

No, there are no required monthly payments.

Interest does accrue, and if the loan is never repaid, the balance is deducted from the death benefit. Many people choose to repay loans to maintain flexibility and reduce long-term costs.

Why not just use a bank or invest the money instead?

Banks provide liquidity but very little growth. Investments can provide higher returns but come with volatility and less predictable access to capital.

Infinite banking sits between the two, offering steady growth with flexible access to money.

Is infinite banking better than investing?

It’s not a replacement for investing.

It’s a way to manage cash flow and keep capital growing while still using it. Many people use it alongside other investments, not instead of them.

What’s the biggest downside of infinite banking?

The biggest drawback is the slow start.

Early on, your liquidity is limited compared to what you’ve put in. It also requires consistency and a long-term approach to work effectively.

Final Thoughts about Infinite Banking

Infinite banking becomes much easier to understand once you see it in action.

At its core, it’s not about chasing the highest return or replacing every other financial tool. It’s about changing how your money behaves—so it can continue growing even while you use it.

For the right person, that trade-off makes sense. It offers stability, flexibility, and control over how capital is stored and accessed.

For others, especially those looking for fast growth or short-term liquidity, it may not be the right fit.

The key is understanding what it does well—and what it doesn’t.

Once you see that clearly, it’s easier to decide whether it belongs in your overall financial strategy.

Want to see how this might work for you?

→ Schedule a call with our team

→ Explore the full Infinite Banking blog archive

Don't Miss Out on Transforming Your Financial Future. Enroll Today!

© Copyrights by ULC. All Rights Reserved.