Most people don’t realize this, but you don’t have a money problem—you have a banking problem.

Most people aren’t broke because they don’t make enough money. They’re broke because they don’t control the system their money flows through.

Every time you borrow money, you’re paying interest to someone else. Every time you save money, you’re earning less than what that same institution charges borrowers. That gap is where banks make their profit—and where most people quietly lose wealth over time.

That’s why strategies like Infinite Banking and Velocity Banking have become increasingly popular. Both are built around a simple idea: take back control of your banking so you stop losing money to interest.

But here’s where most people get confused.

These two strategies are often lumped together under the phrase “becoming your own banker,” but they are not the same thing—and using the wrong one for your situation can cost you years of financial progress.

- Infinite Banking is a long-term wealth strategy that uses specially designed whole life insurance to build a pool of capital you control.

- Velocity Banking is a short-term cash flow strategy that uses lines of credit to aggressively eliminate debt and reduce interest costs.

They solve different problems. They require different levels of discipline. And they carry very different risks.

If you’re trying to decide between Infinite Banking vs Velocity Banking, the real question isn’t “which one is better?”

It’s:

Are you trying to eliminate debt as fast as possible—or build wealth that compounds for decades?

In this guide, I’ll break down exactly how each strategy works, where they succeed, where they fail, and how to decide which one actually fits your financial situation.

The Math Behind Infinite Banking vs Velocity Banking

Most articles explain these strategies at a high level.

But if you don’t understand the numbers, you don’t understand the tradeoffs.

Let’s break it down with simple examples.

Infinite Banking: How the Compounding Actually Works

Let’s say you fund a properly designed whole life policy with:

- $10,000 per year

- An average long-term return of about 4.5% (guarantees plus dividends)

After 20 years, you’re not just saving money—you’re compounding it.

A rough outcome looks like this:

- Total contributions: $200,000

- Cash value: approximately $300,000 or more, depending on the policy and dividend performance

Now here’s the key difference.

Let’s say in year 10, you borrow $50,000 for an investment or major purchase.

In a normal account:

- Your balance drops

- You only earn interest on what remains

In Infinite Banking:

- Your full balance continues compounding

- The $300,000 keeps growing, even while you’re using $50,000 elsewhere

That’s the core advantage.

Your capital keeps working, even when you use it.

Velocity Banking: The Interest Savings Math

Now look at Velocity Banking.

Assume you have:

- $25,000 in credit card debt at 18% interest

- Minimum payments that stretch payoff over 10 or more years

Instead, you use:

- A HELOC at 8%

You pay off the credit card immediately and redirect your income to eliminate the HELOC.

Here’s what happens:

- You replace 18% debt with 8% debt

- You aggressively reduce principal using your cash flow

- You eliminate the balance in about 2 to 3 years instead of a decade

The “return” here is not investment growth.

It’s interest avoided.

Avoiding 18% interest is effectively the same as earning an 18% return on your money.

That’s powerful, but it doesn’t last forever.

Once the debt is gone, the benefit stops.

The Key Mathematical Difference

This is where people get confused.

Infinite Banking builds a compounding asset that continues to grow over decades.

Velocity Banking creates a one-time efficiency gain by eliminating expensive debt.

One keeps working indefinitely.

The other stops once the job is done.

A Simple Way to Compare Them

Think of it like this.

Velocity Banking plugs the leak in your financial bucket.

Infinite Banking builds a reservoir that fills over time.

If you’re losing money to high-interest debt, fixing the leak matters most.

But once the leak is fixed, you still need a system to store and grow your capital.

Where the Math Can Break

This is the part most people ignore.

Velocity Banking breaks when:

- Interest rates rise significantly

- Income drops

- Spending increases

If your HELOC climbs from 8% to 10% or higher, the advantage shrinks quickly. If your cash flow tightens, the strategy stalls.

Infinite Banking breaks when:

- The policy is poorly designed

- You borrow heavily and don’t repay

- You stop funding it too early

In that case, the compounding never has time to work in your favor.

The Real Insight

Velocity Banking is about rate arbitrage and cash flow timing.

Infinite Banking is about long-term capital efficiency and control.

They are not competing strategies.

They solve different financial problems.

Understanding the "Becoming Your Own Banker" Movement

At its core, the "Becoming Your Own Banker" movement is a philosophical shift.

It stems from the realization that you don’t just have a "debt" problem or a "savings" problem—you have a "banking" problem.

Every time you buy a car, a house, or a piece of equipment, you are either paying interest to a bank or giving up the interest you could have earned if you had kept your cash invested. This is known as opportunity cost.

The Philosophy of Financial Control

The philosophy here is simple: you should own the pool of capital you use to finance your life.

By becoming the banker, you stop the "leakage" of interest out of your household and redirect it back into your own pocket.

Whether you choose Infinite or Velocity banking, the mindset is the same: treat your personal economy with the same rigor a bank treats its balance sheet.

You are moving from a consumer mindset to a capitalist mindset.

What is Infinite Banking? (The Privatized Banking System)

Infinite Banking, often called IBC (Infinite Banking Concept), was popularized by R. Nelson Nash and is frequently discussed on every major finance podcast.

It is a long-term play focused on building a private reserve of capital for long-term wealth that grows regardless of what the stock market or the local bank decides to do in the short-term or medium-term.

It isn’t just a savings account; it’s a systematic way to warehouse wealth.

The Engine: Dividend-Paying Whole Life Insurance

The "engine" of Infinite Banking is a very specific financial product: a dividend-paying Whole Life Insurance policy issued by a mutual company.

This is not the "off-the-shelf" policy your local agent might pitch.

It is custom-designed (typically with a "Paid-Up Additions" rider) to maximize cash value growth in the early years rather than maximizing the death benefit.

Because mutual insurance companies are owned by the policyholders, not shareholders, you receive dividends.

While not guaranteed, many of these companies have paid dividends every year for over a century, even through the Great Depression and the 2008 financial crisis.

How the Strategy Works in Practice

When you practice IBC, you pay premiums into your policy, which builds up cash value.

When you need money—say, for a new car or a real estate investment—you don’t withdraw the money. Instead, you take a policy loan from the insurance company, using your cash value as collateral.

The insurance company cuts you a check from their funds, while your money stays inside the policy.

You then set up a repayment schedule to pay back the loan to the insurance company, essentially acting as your own lender.

The Power of Uninterrupted Compounding

This is where the magic happens.

Because you didn't withdraw your money—you merely collateralized it—your entire cash value continues to earn dividends and guaranteed interest as if you hadn't touched a dime.

Imagine you have $50,000 in your policy and you "borrow" $20,000 for a car.

In a traditional checking account or savings vehicle, you’d only earn interest on the remaining $30,000.

In an Infinite Banking policy, you continue to earn interest and dividends on the full $50,000. This "uninterrupted compounding" is the mathematical Holy Grail of IBC.

Over decades, this creates a snowball effect that is incredibly difficult to match with traditional savings.

What is Velocity Banking? (The Cash Flow Accelerator)

If Infinite Banking is a marathon, Velocity Banking is a sprint.

It is a cash-flow management strategy designed to wipe out amortized debt (such as mortgages and student loans) in a fraction of the time it would take with standard methods, without necessarily increasing your income.

The Engine: Lines of Credit (HELOCs or PLOCs)

The engine for Velocity Banking is a revolving line of credit—most commonly a Home Equity Line of Credit (HELOC), a Personal Line of Credit (PLOC), or even a high-limit credit card.

Unlike a traditional loan where you get a lump sum and pay it back over time, a line of credit is a "vessel" you can move money into and out of repeatedly.

The Strategy: Using Debt to Cancel Interest

The strategy works through "mathematical leverage."

Traditional loans use amortization, where the bank front-loads the interest. In the early years of a 30-year mortgage, almost none of your payment goes to the principal.

In Velocity Banking, you take a chunk of your line of credit (say $10,000) and make large principal payments on your mortgage.

You then divert your entire paycheck into that line of credit. Your income sits in the HELOC, driving down the daily average balance—which is how interest is calculated on lines of credit—and you pay your monthly expenses out of the HELOC as they come due.

By keeping your "idle" money sitting against your debt, you minimize monthly interest payments and accelerate the principal pay-down.

The Importance of Positive Cash Flow

Velocity Banking does not work if you are living paycheck to paycheck without a stable income.

It requires "discretionary income" or positive cash flow.

The more money you have left over at the end of the month, the faster the "velocity" of your money. If you spend everything you earn, moving money into a HELOC is just moving debt from one pocket to another.

But if you have a surplus, you can use that surplus to cancel out thousands of dollars in mortgage interest, maximizing your total interest savings.

Head-to-Head Comparison: Infinite Banking vs. Velocity Banking

Both strategies involve using credit to your advantage, but they serve different masters.

The Primary Objective: Wealth Building vs. Debt Reduction

Infinite Banking is primarily a wealth-building and legacy tool. Its goal is to create a perpetual motion machine of capital that you can use, recycle, and pass down to the next generation tax-free.

Velocity Banking is a debt-elimination and cash-flow tool. Its goal is to get you to "zero" as fast as possible. It’s about efficiency and freeing yourself from the shackles of long-term interest.

Liquidity and Access to Capital

In Infinite Banking, your liquidity is high but requires patience. It takes a few years for the cash value to build up enough to be useful. However, once established, that liquidity is "guaranteed."

The insurance company is contractually obligated to lend you the money.

In Velocity Banking, your liquidity is tied to a bank’s whim. A bank can freeze or close a HELOC at any time (as many did during the 2008 crash).

If your strategy relies on having access to that line of credit and the bank shuts it down, you could find yourself in a tight spot.

Risk Profile and Margin for Error

Infinite Banking is relatively low-risk.

The "downside" is the slow start and the commitment to premiums. As long as you pay your premiums and manage your loans, the math is guaranteed to work.

Velocity Banking has a higher risk profile.

It relies on variable-interest rate products (HELOCs). If interest rates spike while you are carrying a large balance on your line of credit, the strategy becomes less effective.

It also requires extreme discipline; if you use the line of credit for a shopping spree instead of debt cancellation, you’ve just added more high-interest debt to your plate.

Tax Implications and Long-Term Benefits

Infinite Banking wins on tax efficiency and long-term estate planning.

Cash value grows tax-deferred, loans are tax-free, and the death benefit passes to heirs tax-free. It’s a "triple-tax-advantaged" environment.

Velocity Banking has fewer direct tax benefits.

While it helps you pay off a mortgage faster, it doesn't provide a tax-sheltered environment for growth.

Its "return" is the saved interest, which is powerful, but it doesn't create a transferable asset in the same way IBC does.

Infinite Banking vs Velocity Banking (Comparison Table)

The Simple Way to Think About It

- Velocity Banking clears the path by eliminating debt and freeing up cash flow

- Infinite Banking builds the system by turning that cash flow into long-term wealth

One is about speed. The other is about control.

Which Strategy Wins for Your Specific Goals?

There is no "winner" in a vacuum—only the strategy that wins for you.

Scenario A: You are focused on aggressive debt elimination

If you are staring down a $300,000 mortgage and it’s keeping you up at night, Velocity Banking is your tool.

It is designed to take a 30-year sentence and turn it into a 7- to 10-year project.

If your primary goal is to be debt-free so you can finally start breathing, start here.

Scenario B: You want to build a legacy and supplement retirement

If you already have your debt under control and you are looking for a way to protect your wealth from market volatility and taxes, Infinite Banking is the clear choice.

It allows you to build a "private pension" that you can tap into during retirement while leaving a massive, tax-free legacy for your children.

Scenario C: You are an investor looking for "opportunity funds"

If you are a real estate investor or business owner, Infinite Banking is often the superior choice.

It allows you to use the same dollar twice: once to grow inside the policy, and once (via a policy loan) to buy a flip or a piece of equipment.

You aren't just "saving" interest; you are creating a capital warehouse that you control, regardless of whether a bank thinks you’re "creditworthy" that month.

Can You Use Both? The Hybrid Approach

The most sophisticated financial strategists don’t choose; they integrate. Using both strategies in tandem can create a powerful financial ecosystem.

Using Velocity Banking to Fund an Infinite Banking Policy

A common "Advanced" move is to use Velocity Banking to create the cash flow necessary to fund a large Infinite Banking policy.

You can use a HELOC to pay the annual premium of a Whole Life policy in a lump sum. You then use your monthly cash flow to aggressively pay down the HELOC (Velocity Banking).

Once the HELOC is back to zero, you've successfully moved equity from your home into a tax-advantaged insurance policy.

You’ve traded "lazy equity" in your house for "working equity" in your policy.

Critical Considerations Before You Start

Neither strategy is a "get rich quick" scheme. They both require a level of financial literacy and discipline that the average consumer lacks.

The Cost of Whole Life Premiums

Infinite Banking requires a significant commitment to premium payments and depends on your initial insurability.

These policies are not cheap, and in the first two to three years, you may feel like you’re "losing" money because the commissions and insurance costs eat up the early premiums.

You have to have a long-term horizon (10+ years) for IBC to make sense.

The Dangers of Variable Interest Rates in Velocity Banking

We lived through a decade of record-low interest rates, which made Velocity Banking look like a miracle.

However, as rates rise, the gap between your mortgage rate and your HELOC rate narrows.

If a HELOC hits 9% or 10%, the math of using it to pay off a 4% mortgage starts to become less attractive.

You must run the numbers based on current rates, not 2020 rates.

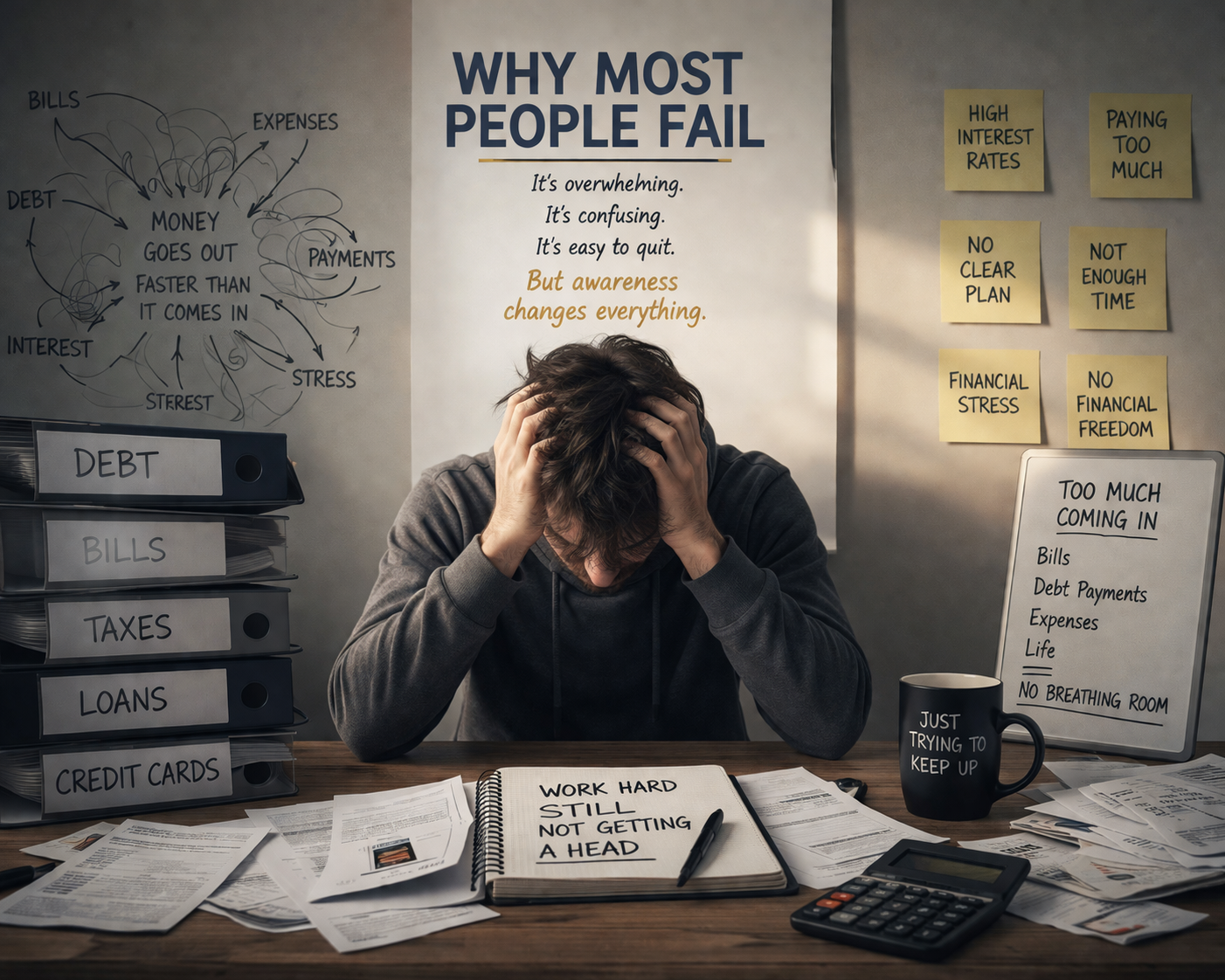

The Discipline Factor: Why Most People Fail

The biggest threat to these strategies isn't the math; it's the person in the mirror.

- Velocity Banking requires you to look at a $50,000 line of credit and not see "spending money."

- Infinite Banking requires you to "honestly" pay back your policy loans even though there is no collector hounding you.

If you struggle with overspending, these strategies can actually make your situation worse by turning a potential asset into a significant liability.

Both Infinite Banking and Velocity Banking look powerful on papera—and they are.

But most people don’t fail because the math doesn’t work. They fail because of behavior.

These strategies require a level of discipline that most people simply don’t have.

Velocity Banking Fails Loudly

Velocity Banking looks like a math strategy, but it’s really a behavior strategy.

On paper, it works beautifully.

- Lower interest rate

- Aggressive principal reduction

- Faster payoff timeline

But in real life, people:

- Keep spending

- Treat the line of credit like free money

- Lose income or consistency

And suddenly, what was supposed to eliminate debt just becomes a new layer of debt. What was supposed to get you out of a hole only made it deeper.

If you don’t have strict control over your cash flow, Velocity Banking doesn’t fix your problem.

It exposes it.

Infinite Banking Fails More Quietly

Infinite Banking doesn’t blow up.

It just underperforms.

People fail with it when they:

- Buy poorly structured policies

- Underfund the policy

- Borrow against it and never repay

- Quit after a few years because it feels slow

And that last one is the most common.

Infinite Banking requires patience because the first few years feel like nothing is happening.

If you don’t understand the long-term nature of compounding, you’ll quit before it starts working in your favor.

The Real Risk Isn’t the Strategy

It’s you.

Both strategies assume something most people don’t have:

- Consistent income

- Controlled spending

- Long-term thinking

Without those, neither strategy works.

The Hard Truth

Velocity Banking is powerful—but fragile.

Infinite Banking is stable—but slow.

Most people want something that is:

- fast

- easy

- and guaranteed

Neither of these strategies gives you that.

What Actually Works

The people who succeed with these strategies all have one thing in common:

They treat their personal finances like a system—not a series of hacks.

They:

- control their spending

- understand their numbers

- follow through consistently

Because at the end of the day, no strategy can outperform bad behavior.

Expert Verdict: Choosing the Right Path

If you are just starting your journey and are burdened by high-interest consumer debt or a massive mortgage, Velocity Banking is the most effective way to "clear the deck."

It provides immediate psychological and mathematical wins by destroying debt, making it a premier debt payoff tool.

However, if you are looking for the ultimate "end-game" strategy—the one used by the wealthiest families in America to protect and grow their fortunes across generations—Infinite Banking is the gold standard.

It creates a level of stability, tax protection, and compounding growth that a line of credit simply cannot match.

The "winner" is the strategy you will actually stick to for your financial future.

Velocity Banking is a sprint to the finish line of debt; Infinite Banking is the construction of a fortress that lasts a lifetime.

If you want to learn more about building your own bank, becoming your own banker, and the Infinite Banking concept, talk to us here.

Common Questions About Banking Strategies

Is Infinite Banking a scam?

No, but it is often "missold." Infinite Banking is based on the standard mechanics of Whole Life Insurance, which has existed for over 150 years. The "scam" aspect usually comes from agents who don't structure the policies correctly or who promise unrealistic returns. When structured properly with a reputable mutual company, it is a legitimate and powerful financial tool.

Do I need a high credit score for Velocity Banking?

Yes. Since Velocity Banking relies on your ability to open and maintain a high-limit Line of Credit (HELOC or PLOC), your credit score and debt-to-income ratio are critical. If your credit is poor, you won't be able to get the "engine" you need to start the strategy.

How soon can I see results?

With Velocity Banking, you see results almost instantly in the form of reduced interest charges and a rapidly dropping principal balance. With Infinite Banking, the results are slower. It usually takes 4 to 6 years to reach the "break-even" point where your cash value equals the premiums you've paid. From that point on, the growth accelerates exponentially.