How IBC takes back power from the banks

Traditional banking has a number of problems, but one that Infinite Banking solves is that it's built on the idea of "interest spread." That is, banks prioritize institutional profit over —and at the expense of—the growth of consumers' money. Your money.

While banks provide a valuable service—namely, a place to store your hard-earned money so it doesn't rot in the backyard when you bury it, along with a reasonable degree of security—practitioners of the Infinite Banking Concept (IBC) believe that the price you pay for this service exceeds the value gained from it.

By dictating the terms of your liquidity and credit, traditional banks essentially "rent" your own financial potential back to you, keeping you trapped in a cycle of compounding debt rather than compounding wealth. Initially, it does not appear this way, but if you peek under the hood and take the time to understand what's really going on, then the problem becomes so obvious that you'll feel as if the banks have been ripping you off.

And that's because, in a very real sense, they have.

The following walks you through how the Infinite Banking Concept works, but if you want to see a real example with numbers, read this article here. This article also tells a great story of how it worked in a client's life.

The problem: You lose money so banks can profit

For example, let’s say John borrows $300,000 to buy his house at a 6% interest rate. That means John is paying about $18,000 in interest per year at the beginning of the loan (6% of $300,000).

Over time, as he pays down the loan, the interest amount slowly decreases—but early on, most of his payments go toward interest. That $18,000 doesn’t just disappear. It goes to the bank.

The bank collects all the interest it earns—from John and thousands of other borrowers—and pools it. Then it pays a small portion of that out to people like you who have money sitting in savings accounts.

So if you have $10,000 in a savings account earning 1% interest (a very generous interest rate for a standard savings account, but we’re simplifying for the example), you’ll make about $100 per year [2]. John pays $18,000 in interest. You get $100. The bank keeps the difference.

Even if we simplify it to say the bank pays out 1% to all depositors while charging borrowers 6%, that 5% spread is where the bank makes its money. They’re using your money to earn a much higher return than what they give you.

So while your money is working, it’s mostly working for the bank—not for you. That’s already bad enough, but it gets even worse from your perspective. When you need money that exceeds the value of your savings—like for a car, a house, education, or a medical emergency—you go back to the bank and ask to borrow [16].

If they approve you, they lend you money and charge you interest. So the bank is making money when you deposit your cash and when you borrow it back.

No matter what side of the deal you’re on, you have to pay. The bank makes money either way.

He who controls the bank maketh the rules

You’re playing by their rules, not yours. The bank dictates when you can borrow, how much you can borrow, and exactly what interest rate you’ll be forced to pay on what you borrow. If your credit score doesn't meet their shifting standards, they can shut the door on you entirely.

Inflation outpaces the rate of growth on your money

The “growth” on traditional savings is a comforting lie; after inflation, your purchasing power actually shrinks. As of March 2026, the national average for traditional savings sits at a dismal 0.39% APY [1]. Meanwhile, the Consumer Price Index (CPI)—the standard measure of inflation—was reported at 2.4% for February 2026 [8].

When your bank pays you 0.39%, but the cost of goods rises by 2.4%, you are experiencing a negative real interest rate of -2.01% [11]. In practical terms, this means that even though your account balance is technically increasing, the 'real' value of that money is evaporating.

For example, a $500 smartphone today is projected to cost roughly $512 by next year due to inflation; however, that same $500 in a traditional savings account would only grow to $501.95, leaving you over $10 short of the same purchase [12]. Without moving funds to an account that at least keeps pace with current inflation, your savings are effectively losing a race against time.

While moving to a High-Yield Savings Account (HYSA) can boost that return to 5% APY—nearly 15 times the average—that extra yield isn't free [4]. It comes tethered to a web of restrictions and logistical hurdles that make these accounts impractical, or even out of reach, for many everyday consumers.

The Reality Check: Why HYSAs Aren’t for Everyone

While that 5% headline looks great on a billboard [4][6], here is why most people struggle to actually make an HYSA work for their daily lives:

The 'Digital-Only' Barrier: Most HYSAs are offered by online-only banks. For the millions of Americans who use physical cash—like tipped workers and small business owners—these accounts are a nightmare. You can’t drive to a branch and deposit a stack of twenties; you have to deposit them at a local bank first, wait for the funds to clear, and then initiate an electronic transfer.

The Liquidity Lag: In a true emergency, you need money now. If your car breaks down on a Saturday, a traditional bank lets you walk into a branch or hit a local ATM. With many HYSAs, moving money back to your "real world" checking account can take two to three business days. That delay is a luxury many families living paycheck to paycheck simply can't afford.

The 'Hoop-Jumping' Requirements: To get that top-tier 5% rate, banks often hide the fine print [3][29]. You might be required to have at least $1,000 in monthly direct deposits or maintain a $5,000 minimum balance. If your balance dips because of an unexpected bill, the bank might drop your interest rate to nearly zero or hit you with a maintenance fee that wipes out all the interest you earned that month [5].

The Psychological Friction: Because these accounts usually lack a debit card or the ability to write checks, they are "siloed." While this helps some people save, it creates a massive hurdle for the average consumer who needs their money to be interchangeable and immediate. When life happens fast, the "high yield" isn't worth the "high hassle."

Regulation D: Historically, this federal rule strictly limited consumers to just six withdrawals per month from savings accounts, with banks required to penalize or even close accounts that exceeded the cap [7]. While the Federal Reserve officially deleted these numeric limits in April 2020 to provide greater financial flexibility, the change was permissive rather than mandatory [7].

This means that as of 2026, many banks have chosen to keep these restrictions in place as internal policy. For consumers, this creates a 'hidden' trap: you may still face transaction fees of $5 to $15 per withdrawal, despite the federal government no longer requiring them.

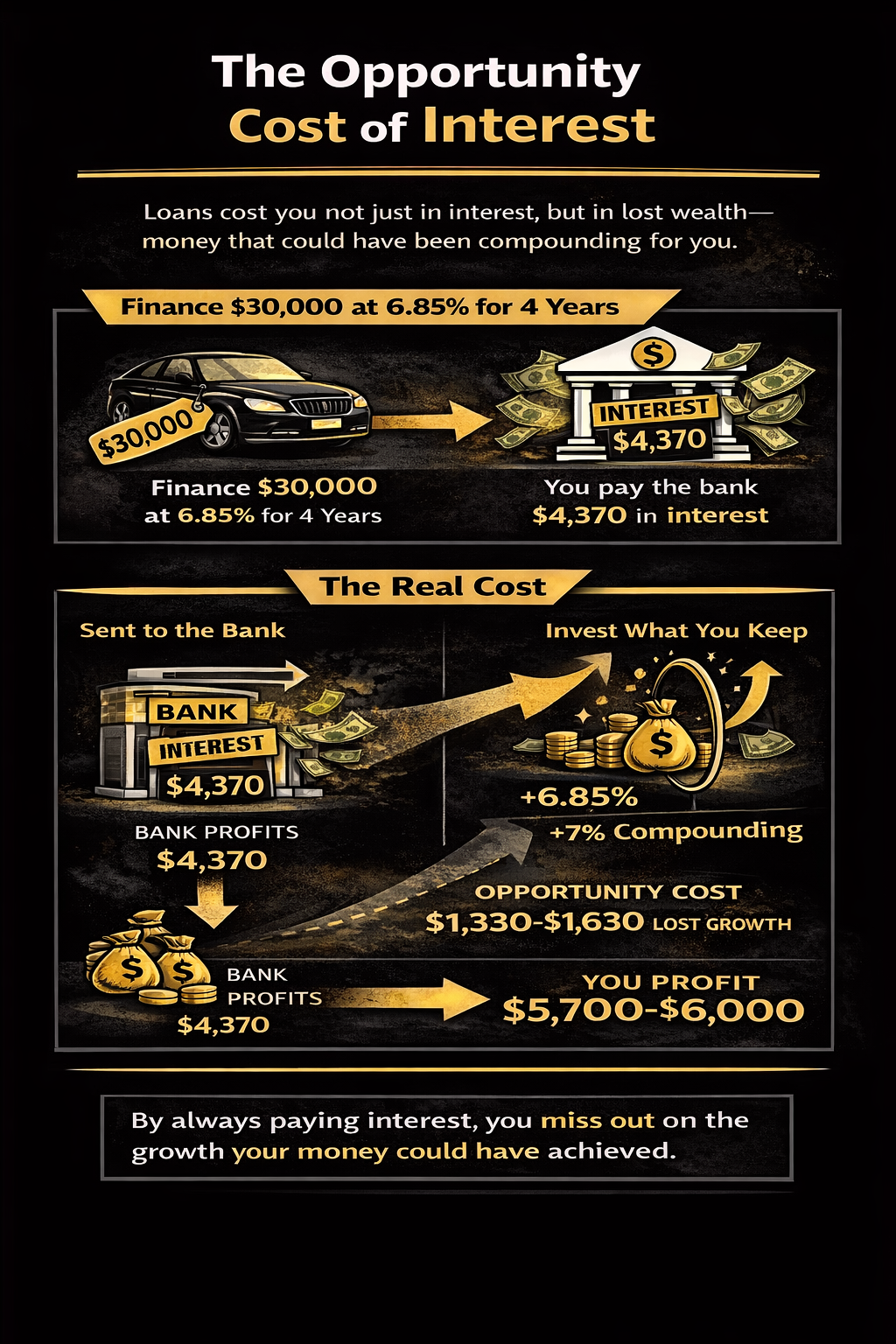

The opportunity cost of interest

Another flaw is how interest works against you in a cycle of compounding debt. Every time you take out a loan, you’re paying interest to someone else—basically renting their money. But the real cost isn’t just the interest you see on paper; it’s what that money could have done for you if you had kept it [15].

Let’s use a simple example. As of March 2026, the average interest rate for a 48-month used car loan is about 6.85% [13]. If you finance $30,000 at that rate, you’ll pay roughly $4,370 in interest over four years. That $4,370 is money that leaves your control and goes to the bank.

Now imagine instead that you kept that same $4,370 and invested it, earning a modest 7% return [28]. After four years, it would grow to around $5,700–$6,000. So the real cost of that loan isn’t just $4,370. It’s closer to $6,000 when you include the growth you missed out on.

That may not sound like a huge difference—but here’s where it adds up. Most people don’t just take out one loan. They finance cars, carry credit cards, and take personal loans—often at rates significantly higher than a standard auto note [14][16]. Each time, they’re sending money out in interest and losing what that money could have become.

Over decades, this creates a pattern: money constantly flowing away from you instead of compounding for you. Traditional banking keeps you in that cycle—paying interest, over and over again.

Infinite Banking: How we become our own bank

With Infinite Banking, the goal is to keep more of that money within your own system instead of giving it away. To understand how we do that, you first have to understand whole life insurance [18].

Whole Life Insurance vs Term Life Insurance

To understand why whole life insurance is the engine behind "infinite banking," you have to understand the differences between the life insurance typically purchased (“term life insurance”) versus what the Infinite Bank Concept uses instead (“whole life insurance”) [17].

Term Life Insurance (The "Rental"): You pay a low monthly premium for a specific period (e.g., 20 years). If you die during that time, your family gets a payout. If you outlive the term, the policy expires, and you walk away with zero [19]. There is no "bank" to build because there is no cash value [22].

Whole Life Insurance (The "Equity"): This is a permanent asset that stays with you for your entire life [21]. While the premiums are higher, they are fixed—they never go up [20]. Most importantly, every payment you make builds equity (cash value) that you can actually use while you are still alive [17].

Why Whole Life Insurance is the Ideal "Bank" Vehicle

For a financial system like infinite banking to work, your "vault" needs specific characteristics that only properly structured whole life policies provide [17, 18]:

Guaranteed Capitalization: Unlike the stock market, your cash value is contractually guaranteed to grow every single year [19, 21]. It creates a "floor" that prevents your bank from ever losing value during a market crash [17]. It also makes your capital less susceptible to global stock market fluctuations, which historical averages show can be volatile despite long-term gains [28].

Uninterrupted Compounding: When you "borrow" from your policy, you aren't actually withdrawing your money; you are taking a loan from the insurance company and using your cash value as collateral [18, 31]. Because your money stays inside the policy, it continues to earn interest and dividends on the full amount as if you hadn't touched it [30, 31].

Private Liquidity: You are the loan officer; there is no credit check, no income verification, and no lengthy bank approval process to access your funds [17, 18]. You decide the repayment terms, giving you total control over your cash flow [18].

Tax-Advantaged Growth: The interest and dividends grow tax-deferred, and policy loans are typically received tax-free [23, 26, 32]. This allows you to bypass the "tax drag" that slows down traditional savings accounts and HYSAs, where interest is taxed as ordinary income [11, 27].

Specific Conditions Affecting Tax-Free Policy Access

The following section is a little heavier on the financial jargon, but it’s important to read because it sets the honest expectation of what exactly Infinite Banking can—and can not—do. It’s not a magic money cheat code or tax evasion strategy, and understanding the following section will ensure that you enter the Infinite Banking apparatus with misplaced ideas of what’s possible.

There are some conditions that apply to the infinite banking concept that will nullify its primary advantage: tax-deferred growth. It’s important to be aware of these conditions when building your bank so you can obtain the maximum benefit.

The MEC Trap (Modified Endowment Contract)

If a policy is funded too aggressively, it may fail the 7-Pay Test—a calculation mandated by IRC Section 7702A that limits the amount of premium paid within the first seven years [1, 6, 11].

When this happens, the IRS reclassifies the contract as a Modified Endowment Contract (MEC), removing its status as an insurance product and treating it as an investment vehicle [16, 19, 20].

LIFO Taxation: Unlike a standard policy, MEC distributions (including loans and withdrawals) are taxed on a "last-in, first-out" (LIFO) basis, meaning any internal gains are taxed as ordinary income before you can access your original principal [1, 4, 15].

Early Withdrawal Penalty: If you are under age 59½, the taxable portion of any MEC distribution may also be subject to a 10% IRS penalty [1, 4, 14].

Policy Lapse with Outstanding Loans

This is often cited as a significant "hidden" risk in the IBC strategy [32].

If a policy has a large outstanding loan balance and subsequently lapses or is surrendered—typically because rising loan interest exceeds the remaining cash value—the IRS treats the unpaid loan as a constructive distribution [14]. Any amount of that "distribution" that exceeds your policy basis (the total premiums you have paid) is taxed as ordinary income in the year of the lapse [14].

Direct Withdrawals Exceeding Basis

While policy loans remain generally tax-free, direct withdrawals (partial surrenders) follow a "first-in, first-out" (FIFO) rule for non-MEC policies [1, 4, 10]. This means you can withdraw funds tax-free up to the amount of your total premiums paid (your basis) [1, 25]. However, every dollar withdrawn above your basis is treated as a gain and taxed as ordinary income [10, 14, 25].

Transfer for Value Rule

The tax-free nature of life insurance proceeds, including potentially the favorable treatment of loans and the eventual death benefit, can be compromised if a policy is sold or transferred to another party for "valuable consideration" [31].

Under the Transfer for Value Rule, if a policy changes hands for something of value, the tax-exempt status of the death benefit may be limited to the amount paid for the policy plus subsequent premiums, potentially turning a tax-free legacy into a taxable event.

As long as you play by the rules, Infinite Banking can change your life

Assuming that you don’t avoid any of the conditions above that trigger a taxable event, your money does something spectacular.

It’s housed in a savings account with rules that guarantee growth. Over time, that cash value builds into a pool of money you control.

And you can borrow against that money whenever you want, without credit checks or loan applications. And the collateral is built into the whole life insurance policy.

Because you’re not taking money out of the account—you’re borrowing against it, using it as collateral—your full cash value keeps growing in the background as if you never touched it.

So you get two things happening at once:

You have access to money when you need it, and it continues compounding.

This is what makes whole life insurance ideal for Infinite Banking. It gives you a place to store money, grow it at a guaranteed rate, and still use it when opportunities or emergencies come up—without depending on a bank.

And, perhaps most importantly, you have a life insurance policy to cover your loved ones should you meet an untimely demise.

The Strategic Value of Whole Life Insurance

When comparing Whole Life Insurance to the stock market or a High-Yield Savings Account, it is essential to distinguish between a speculative investment and a liquidity-focused asset.

While the S&P 500 has historically returned approximately 10% annually, that yield comes with significant volatility and "sequence-of-returns" risk—the danger that a market drop occurs exactly when you need to access your capital.

Conversely, while an HYSA offers stability and an APY of 4–5%, these returns are fully taxable as ordinary income and are subject to immediate reduction if the Federal Reserve cuts interest rates.

A properly structured whole life policy functions as a "volatility buffer," providing a contractually guaranteed base return (typically 2–3%) plus non-guaranteed dividends that can bring total net yields into the 4–5% range over the long term.

Whole Life Insurance and Infinite Banking Allow You to Be “Two Places At Once”

The primary advantage of a whole life policy for "Infinite Banking" is the Policy Loan feature.

Unlike a bank withdrawal, a policy loan does not remove money from your account. Instead, the insurance company provides a loan using your cash value as collateral.

If the policy is issued by a Non-Direct Recognition carrier, your full cash value continues to earn dividends and interest as if you had never touched it. While you will pay a loan interest rate (currently averaging 4.5% to 6% in 2026), the policy's internal compounding helps offset this cost, allowing your capital to remain in uninterrupted compounding even while it is deployed for outside opportunities.

Is Infinite Banking Right For You?

Infinite Banking is not a "get rich quick" scheme; it is a long-term capital management strategy. It is most effective for:

- High-Income Earners: Those who have already maximized traditional tax-advantaged accounts (401ks/IRAs) and seek additional tax-deferred growth.

- Liquidity Seekers: Individuals who want "private" access to capital without credit checks or bank approval processes.

- Risk-Averse Savers: Those who value a guaranteed "floor" to ensure their primary capital is never subject to market losses.

If you fit any of the above—or you simply want to learn more—schedule a call with at Unlimited Life Concepts.

References

1. Federal Deposit Insurance Corporation. (2026, March 16). National rates and rate caps. https://www.fdic.gov/national-rates-and-rate-caps

2, Federal Reserve Bank of St. Louis. (2026, March 16). National rate: Savings (SNDR). FRED Economic Data. https://fred.stlouisfed.org/series/SNDR

3. Flanagan, G. L. (2026, March 19). Today’s top high-yield savings rates: Up to 5.00% on March 19, 2026. Fortune. https://fortune.com/article/best-savings-account-rates-3-19-2026/

4. Forbes Advisor. (2026, March 19). High-yield savings account rates today: March 19, 2026 – Rates are steady. https://www.forbes.com/advisor/banking/savings/savings-account-rates-today-03-19-2026/

5. NerdWallet. (2026, March 16). Average bank interest rates for savings accounts, CDs and more. https://www.nerdwallet.com/banking/learn/average-rates-for-deposit-accounts

6. The Wall Street Journal. (2026, March 11). Best high-yield savings accounts for March 2026: Up to 5.00%. https://www.wsj.com/buyside/personal-finance/banking/best-high-yield-savings-account

7. Board of Governors of the Federal Reserve System. (2020, April 28). Regulation D: Reserve requirements of depository institutions (Rule 12 CFR Part 204). Federal Register. https://www.federalregister.gov/documents/2020/04/28/2020-09044/regulation-d-reserve-requirements-of-depository-institutions

8. Bureau of Labor Statistics. (2026, March 11). Consumer Price Index news release. https://www.bls.gov/cpi/news.htm

9. CNBC. (2026, March 11). Here's the inflation breakdown for February 2026 — in one chart. https://www.cnbc.com/2026/03/11/cpi-inflation-february-2026-breakdown.html

10. Federal Deposit Insurance Corporation. (2026, March 16). National rates and rate caps. https://www.fdic.gov/national-rates-and-rate-caps

11. Investopedia. (2026, March 11). CPI is still elevated—Here's the rate your savings needs to earn to stay ahead. https://www.investopedia.com/cpi-is-still-elevated-heres-the-rate-your-savings-needs-to-earn-to-stay-ahead-11923899

12. U.S. Congress Joint Economic Committee. (2026, March 11). Inflation update: March 2026. https://www.jec.senate.gov/public/index.cfm/republicans/inflation-update

13. Bankrate. (2026, March 18). Current auto loan interest rates. www.bankrate.com

14. Board of Governors of the Federal Reserve System. (2026, March 6). Consumer credit - G.19. www.federalreserve.gov

15. Investopedia. (2026, March 4). Opportunity cost: Definition, formula, and examples. www.investopedia.com

16. St. Louis Fed. (2026, March 13). Finance rate on personal loans at commercial banks, 24-month loan (TERMCBPER24NS). FRED Economic Data. fred.stlouisfed.org

17. Abrams, J. (2025, December 17). Whole life insurance definitive guide for 2026. Abrams Insurance. https://abramsinc.com/whole-life-insurance/

18. Ascendant Financial. (2026, January 2). Infinite banking vs. whole life insurance. https://www.ascendantfinancial.com/infinite-banking-vs-whole-life-insurance/

19. Guardian Life. (2026, January 29). Term vs. whole life insurance: What's the difference? https://www.guardianlife.com/life-insurance/term-vs-whole

20. Northwestern Mutual. (2024, August 20). Comparing term and whole life insurance. https://www.northwesternmutual.com/life-and-money/term-vs-whole-life-insurance/

21. Prudential Financial. (2025, August 5). Term vs whole life insurance: Key insurance differences. https://www.prudential.com/financial-education/term-vs-whole-life-insurance

22. Ramsey, D. (2025, February 13). Term vs. whole life insurance: What’s the difference? Ramsey Solutions. https://www.ramseysolutions.com/insurance/term-life-vs-whole-life-insurance

23. Internal Revenue Service. (2024). Life insurance & modified endowment contracts (Publication 525). www.irs.gov

24. Investopedia. (2025, November 12). How the 7-pay test works for life insurance. www.investopedia.com

25. Legal Information Institute. (2026). 26 U.S. Code § 7702A - Modified endowment contract defined. Cornell Law School. www.law.cornell.edu

26. The American College of Financial Services. (2025). Taxation of life insurance: Loans and surrenders. www.theamericancollege.edu

27. Western & Southern Financial Group. (2026, January 8). When is life insurance cash value taxable? www.westernsouthern.com

28. Investopedia. (2026, March 4). S&P 500 average return. www.investopedia.com

29. Forbes Advisor. (2026, March 19). High-yield savings account rates today: March 19, 2026. www.forbes.com

30. Guardian Life. (2025, November 19). Guardian announces 2026 dividend for individual life policyholders. www.guardianlife.com

31. Penn Mutual. (2026, March 1). Understanding direct vs. non-direct recognition in life insurance loans. www.pennmutual.com

32. Internal Revenue Service. (2024). Taxation of life insurance proceeds (Publication 525). www.irs.gov